- My total return for 2012 was +9.4% (includes dividends) versus +13.4% for the S&P 500

- My current holdings are:

- Cisco Systems Inc. (CSCO) (write-up here)

- Dolby Laboratories Inc. (DLB) (partial write-up here)

- Kulicke & Soffa Industries Inc. (KLIC) (write-up here)

- I will be posting my first net-net write-up shortly

Tuesday, February 26, 2013

Update

Hello to any wayward readers. It's been quite a while since I last posted, so I thought I'd do a quick update in bullet point form.

Thursday, May 10, 2012

Stock Follow-Up: Cisco Systems, Inc. (NASDAQ:CSCO)

I felt that I should write another small blog post on Cisco Systems, since their quarterly financials were released today and caused over a 10% drop in the share price. I took a quick glance at the numbers and immediately felt that the market is greatly over-reacting to earnings falling short of analyst estimates. Both revenue and gross profit increased slightly over last quarter and more significantly over the year-ago quarter. Profit margins, research and development, and selling/general/administrative costs all stayed stable over the last four quarters. Net income only shrunk slightly over that of last quarter, and earnings per share stayed around the same. Owner earnings actually grew by 12% over last quarter, and there was only a small increase in the number of shares outstanding.

I take all this to mean that my original investment thesis on Cisco still stands, despite the significant drop in share price. Therefore, further purchase of shares would make sense for me, since the long-term fundamentals of the company have changed very little or not at all. I am not concerned that the stock price has dropped by around 17% from my initial entry point. I am still convinced that Cisco has great potential over the long term, and am comfortable with my conviction. I would only take a loss of 17% in value if I were to sell my shares right now, but I don't intend on doing so for a very long time yet.

Disclosure: I am long CSCO.

I take all this to mean that my original investment thesis on Cisco still stands, despite the significant drop in share price. Therefore, further purchase of shares would make sense for me, since the long-term fundamentals of the company have changed very little or not at all. I am not concerned that the stock price has dropped by around 17% from my initial entry point. I am still convinced that Cisco has great potential over the long term, and am comfortable with my conviction. I would only take a loss of 17% in value if I were to sell my shares right now, but I don't intend on doing so for a very long time yet.

Disclosure: I am long CSCO.

Wednesday, May 2, 2012

Stock Analysis: Cisco Systems, Inc. (NASDAQ:CSCO)

I haven't posted a stock analysis in a long time, and I've learned a lot about fundamental analysis since my last "stock analysis". I put that in quotes because my previous analysis mainly involved the use of common ratios and how they fit into a relatively rigid dividend growth investing strategy. More recently, I have begun analyzing stocks based on their income statements, balance sheets, cash flow statements, annual reports, and proxy statements. In addition, I intend to only invest in businesses that I understand. My circle of competence is relatively small, but I am beginning to expand it by learning about a second industry. I have just recently finished a Bachelor of Computer Science degree, and so my only real area of expertise is technology. Tech stocks are unpopular with a lot of Buffett-style value investors because their competitive advantage(s) usually rely on continuous capital expenditures and research and development. With that said, it's still my best area of knowledge and I've done a thorough enough analysis that I am personally comfortable with. So without further ado, I'll dive into my analysis of Cisco Systems Inc.

If you aren't aware, Cisco Systems' core product line is the development of equipment for computer network routing and switching. The entire Internet and all private networks rely on routing and switching equipment, and Cisco is the biggest name for enterprise routing and switching, and a significant competitor in the consumer router space.

All of my numbers-oriented discussion relates to the past four years of annual financial data regarding Cisco. They would be best summarized in a bullet list:

I haven't done extensive research on the quality of Juniper Networks' router and switch products, but I would imagine that they are inferior to those of Cisco based solely on the fact that Juniper Networks has been around since before 2000 and I had never heard of them or seen any of their products in use at various software development positions I've held. This is somewhat anecdotal, but I feel that it is telling of Cisco's brand recognition and large market share.

If you aren't aware, Cisco Systems' core product line is the development of equipment for computer network routing and switching. The entire Internet and all private networks rely on routing and switching equipment, and Cisco is the biggest name for enterprise routing and switching, and a significant competitor in the consumer router space.

All of my numbers-oriented discussion relates to the past four years of annual financial data regarding Cisco. They would be best summarized in a bullet list:

- Consistent gross margin around 64%

- Consistent R&D expense around 22% of gross profit

- Consistent selling/general/admin expense around 42% of gross profit, which isn't a bad percentage

- Net income as a percentage of revenue is consistently above 15%

- Over $44 billion in cash and short-term investments

- Cash/short-term investments plus accounts receivable is consistently around 2 times current liabilities

- Four times annual net income is consistently around 2 times long term debt (could pay off all long term debt within 4 years or less, using only net income)

- Return on assets is 10% on average

- Consistent retained earnings growth

- Return on equity consistently greater than or equal to 14%

- Debt-shareholder equity ratio consistently around 0.8

- Consistent annual decline in shares outstanding by around 3%

- Capital expenditure divided by net income is 16% on average (even 25% or less is good)

- Average annual owner earnings of $8,004 million (Net income + Depreciation/Amortization - Capital expenditure)

The thing you immediately notice about this bullet list is that consistency is mentioned in almost every bullet point. That is why I focused on average values or approximate values, rather than percentage growth or decline year over year, but more on that later. Consistent cost management and return on assets/return on equity make for a pretty dependable stock. Debt is not used in excess, and is manageable in terms of being able to service the debt. Retained earnings growth, share repurchases, and lots of owner earnings are all good signs too.

Another point that I left out to talk about separately is that the company has recently begun paying a quarterly dividend. At the moment, the payout ratio is only 8%, but Cisco has more than enough owner earnings and cash to pave the way for long-term dividend growth. If I start building a position in the stock now to hold over the long term, the dividend yield-on-cost could be significant.

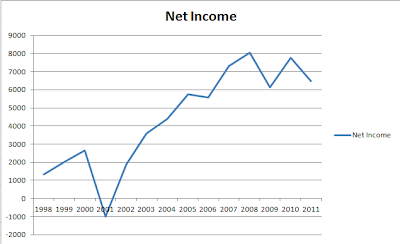

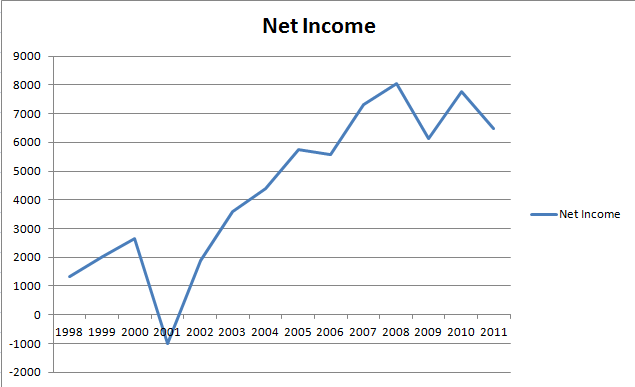

Unfortunately, revenue growth, net income growth, earnings per share growth and owner earnings growth are not consistent year over year, but they do seem to be in a long-term upward trend, despite dips every other year recently. The following chart gives a quick visual of Cisco's net income since 1998:

An investment should not be made based solely on financial statement numbers, and so I will now move on to a discussion of the company's management and macro-economic outlook. To start, I will state some quotes from Cisco's 2011 proxy statement. Out of all the corporate governance policies, three stood out to me as good elements to see in a company:

- "The independent members of the Board of Directors meet regularly without the presence of management" - This is good because there is no pressure on the board to withhold negative comments or constructive criticism of the CEO, which would be the case if he were present. It is the job of the board to evaluate the CEO and reward his performance or lack thereof accordingly.

- "Cisco has adopted a compensation recoupment policy that applies to its executive officers". Further reading in the proxy shows that this comes into effect in the case of a restatement of past financial statements. This motivates the executives to ensure honesty in the financial statements.

- "Cisco has stock ownership guidelines for its non-employee directors and executive officers". In particular, the proxy goes on to say that the CEO is required to own 5 times his base annual salary in Cisco common stock. In reality, "[the] CEO holds over 100 times his base annual salary in Cisco common stock". This means that it is in the interest of the board and the executives to put shareholder interests above all else.

I listened to Cisco's most recent fiscal year-end quarterly conference call, and found the following notes of interest:

- CEO seems to have a good grasp on the technology itself being used in Cisco's router and switch products

- "Intelligent" routers are a main focus of Cisco product development. Coming from a computer science background, I take this to mean that the "intelligence" or routing algorithms are being moved closer to the hardware (the routers themselves). This most likely leads to vast performance improvements in terms of network bandwidth and capacity.

- Cisco customers buy into an entire networking architecture. This makes it easy for customers to upgrade to newer Cisco products as they are developed, and also makes it hard for customers to switch to a different networking architecture from a rival company (due to the amount of time and money it would take).

- Data center trends are moving toward consolidation, virtualization, and private cloud services, all of which Cisco can address with its products. Having worked in software development positions for large private companies, I can see the value that a private cloud would provide for a company's internal intranet, document and source code storage, software compilation and testing, etc.

- Cisco has partnerships with VMware (the biggest virtualization software company) to accomplish these goals.

I don't simply take these statements from the conference call at face value. Because of my understanding of and background in software development and computer science, I can verify for myself that these statements make sense. This is a good example of the importance of investing in a company whose products and services you understand.

In terms of macro-economic trends that would benefit Cisco, I think that the move toward cloud services (both private and provided by 3rd-party companies such as Amazon) will continue to grow. Additionally, the move to Internet Protocol version 6 will necessitate the purchase of equipment that supports the new protocol (which Cisco routers satisfy). The internet in general is constantly growing, and its existing users are constantly demanding faster speeds and more bandwidth. In addition, mobile smartphone growth is also continuing, and network infrastructure is needed to support this growth. For these reasons, I believe that Cisco has a lot of revenue growth potential.

Cisco's closest competitors are Hewlett-Packard and Juniper Networks. I did some quick analysis on Juniper Networks, just to see how competitive they really could be with Cisco. Here are some bullet points that I found over the past 4 years of their financial data:

- R&D costs are consistently above 30% of gross profit

- Much less net income than Cisco (most recently an annual value of $425 million compared to Cisco's annual $6.5 billion)

- Negative retained earnings every year with no discernible upward trend

- Return on equity and return on assets consistently below 10%

- Higher capital expenditure as a percentage of net income on average

One concern that I have about this stock is that Cisco mainly fuels its growth through acquisitions, which can be prone to being more costly than profitable. Cisco has recently announced the end of its Flip Video product line that it acquired several years ago from another company. If many acquisitions are made over time, some of them are bound to turn out badly, to the detriment of shareholders. Luckily, management admits that things turned out badly and discontinues the product line, rather than pumping more money into it. In addition, I believe that Cisco's core router and switch product lines aren't likely to be of such poor quality that earnings will suffer in a significant way.

Finally, valuation of Cisco shares must be considered to see what kind of margin of safety exists at the current price per share. I assumed a conservative growth of owner earnings of 5% annually (although this has the potential to be much higher). Factoring in discounted cash flows over ten years, Cisco's total assets and total liabilities, I came up with a target price/intrinsic value of around $34 per share. As of this writing, Cisco shares closed at $19.84. I have initiated a position and plan to buy more if shares dip even lower in the near future.

Any thoughts on my analysis?

As always, this blog post should not be considered financial advice, and you should always do your own research before making any investment decision. Disclosure: I am long CSCO.

Edit: Click here to read some follow-up thoughts on Cisco Systems after their most recent quarterly earnings release.

As always, this blog post should not be considered financial advice, and you should always do your own research before making any investment decision. Disclosure: I am long CSCO.

Edit: Click here to read some follow-up thoughts on Cisco Systems after their most recent quarterly earnings release.

Subscribe to:

Posts (Atom)